Orchestration Is the Shovel in This Stablecoin Gold Rush

The stablecoin gold rush is real. But like any gold rush, the question isn't who's digging. It's who's selling the picks and shovels.

Saniya More

Julian Rachman

Another day, another stablecoin announcement. It really does feel like everyone's leaning into stablecoins harder than ever. Blockchains like Solana, Base, Tempo, and Plasma are racing to become the rails for digital dollar flows. Annual stablecoin transfer volumes exploded to over $27 trillion in 2024, surpassing the combined volume of Visa and Mastercard for the first time. By early 2025, the on-chain stablecoin supply had swelled past $213 billion (up 53% in 2024 alone). Regulatory clarity like the U.S. GENIUS Act has given banks and fintechs the green light to operate with stablecoins at scale.

The stablecoin gold rush is real. But like any gold rush, the question isn't who's digging. It's who's selling the picks and shovels.

Payment Chains Are Fighting the Wrong Battle

Payment chains today are in a land grab, obsessing over throughput and transaction volume as if it were 2017 all over again. Solana boasts tens of thousands of TPS, new Layer-2s undercut each other on fees, and TVL is chased as the ultimate prize. But this infrastructure arms race hides an uncomfortable truth: blockchain infrastructure is rapidly commoditizing.

Circle's decision to deploy USDC across 28 different blockchains isn't an anomaly. It's proof that the underlying rails are interchangeable. There's always another L2 claiming to be 10% faster or 10% cheaper. Being "the fastest chain" is a short-lived differentiation at best.

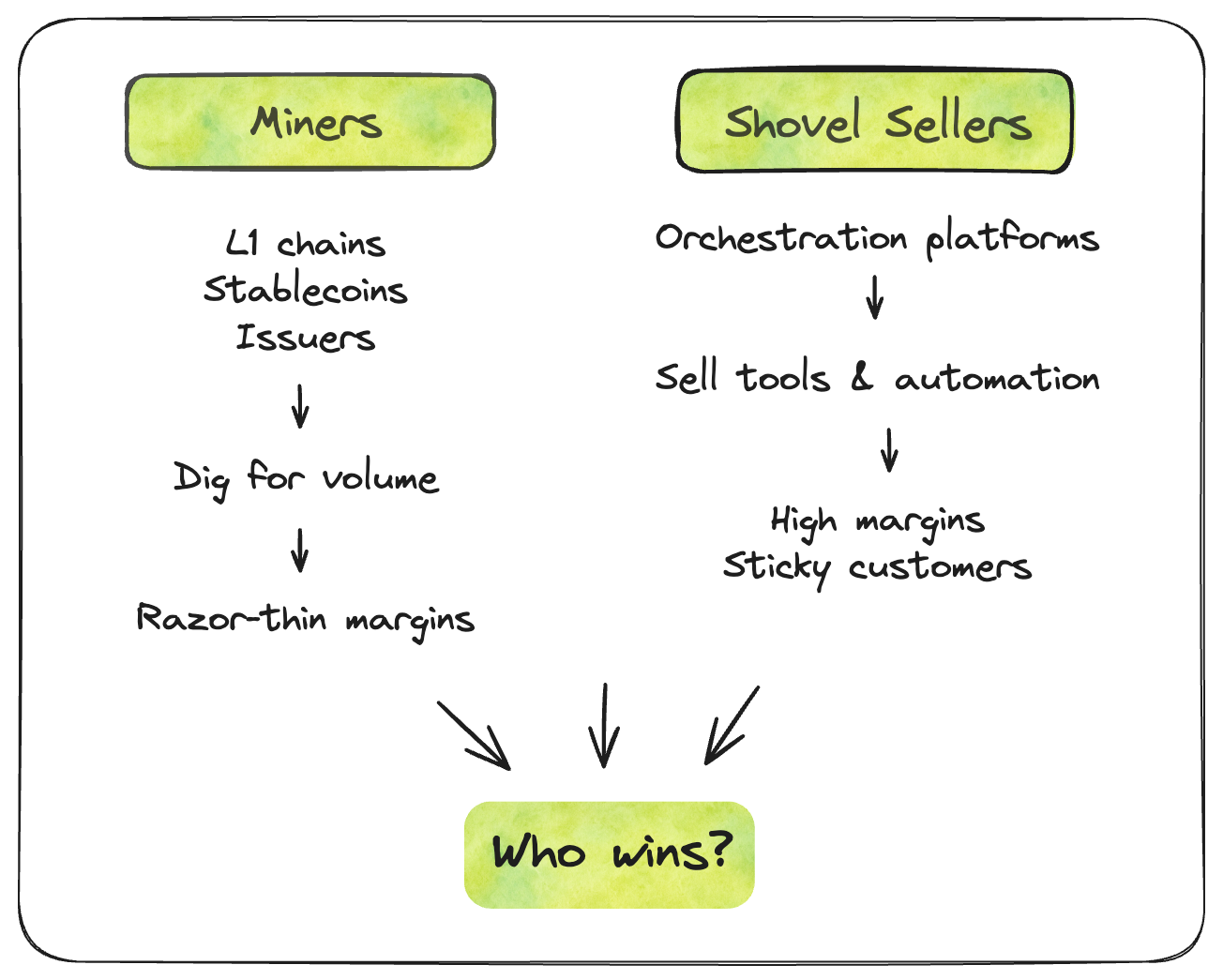

Think about the California Gold Rush. In 1849, folks selling picks and shovels profited more reliably than miners digging for gold. The miners faced uncertain returns and fierce competition. The toolmakers had consistent demand regardless of who struck gold.

Today's stablecoin landscape mirrors this. The L1s and stablecoin issuers are the miners digging for gold (transaction volume and TVL). But today's miners face razor-thin margins and endless competition. When every network can settle a USDC transfer in seconds for pennies, no single chain can maintain a durable edge.

If the chains aren't capturing the lion's share of value, then who is?

Enterprises Want Stablecoins, But They Can't Actually Use Them

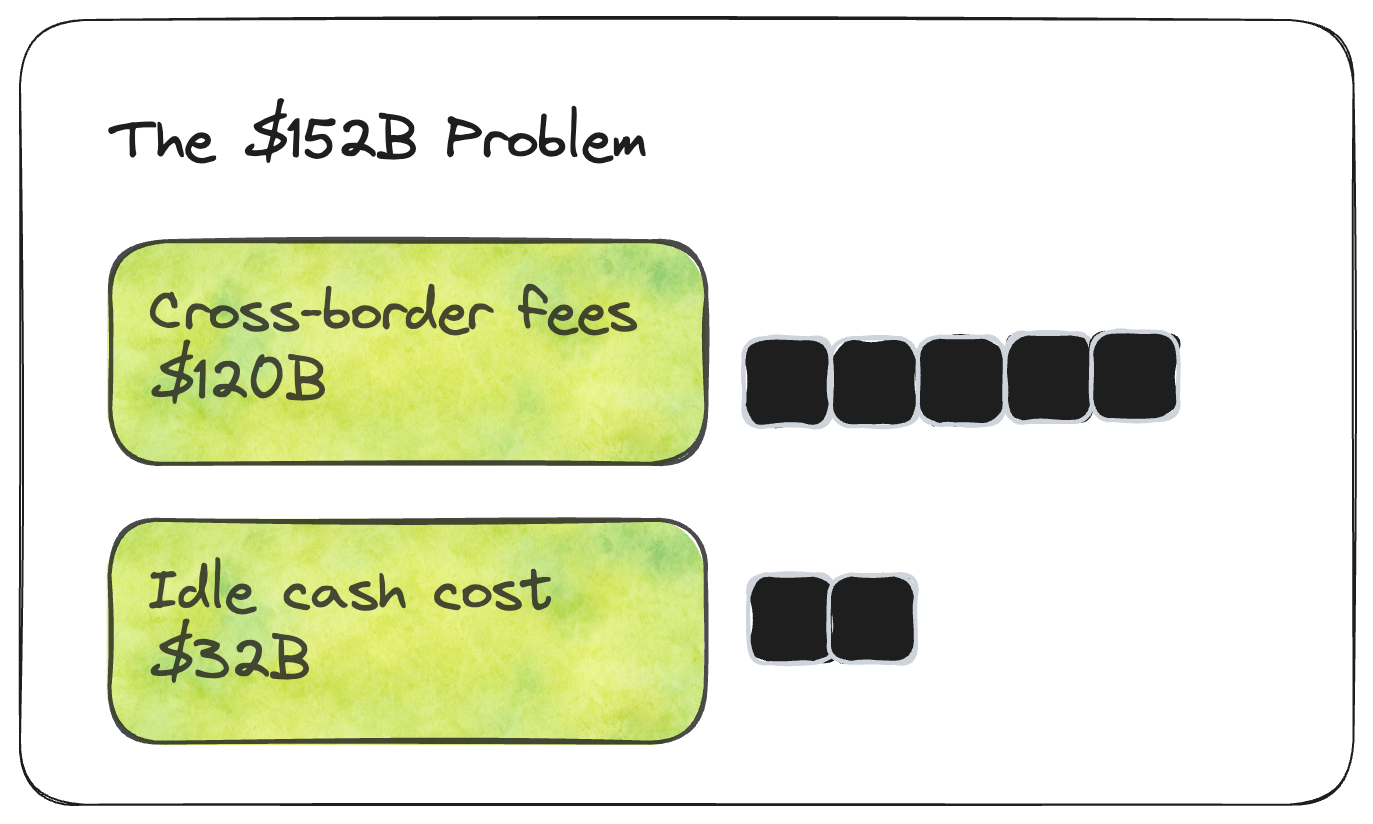

Companies are bleeding massive sums under today's system. Over $120 billion per year is spent on fees and inefficiencies in cross-border payments alone. Additionally, businesses forgo tens of billions in interest by leaving cash sitting idle. Tether earned $13.7 billion in profit in 2024 from interest on reserves, income that could have gone to stablecoin holders.

So why haven't enterprises jumped on stablecoins? Because digital assets today are not plug-and-play.

Sending a stablecoin payment today means navigating a maze of manual steps. You need to configure a wallet, acquire gas tokens, bridge across chains, off-ramp through an exchange, and finally transfer to a bank account. Each step introduces friction and the potential for failure.

Consider a SaaS company trying to bill customers in stablecoins. They manually check each payment, reconcile transactions one by one, and chase down failures when something breaks. With orchestration, the same infrastructure delivers a radically different experience: subscriptions auto-bill, failures trigger smart retries, and everything syncs automatically to their accounting system.

Stablecoins today account for only 0.03% of the $120 trillion global B2B payments market. Not because infrastructure can't handle it, but because infrastructure doesn't integrate with how businesses operate. Payment authorization workflows, invoicing, error resolution, and compliance, all taken for granted in traditional systems, are largely absent in crypto.

The blockers to enterprise adoption aren't technical—they’re operational. This is the gaping hole the current gold rush isn't addressing.

Here's the Pattern Everyone's Missing

The pattern is consistent across tech: infrastructure commoditizes while value moves up the stack. Cloud providers earn more from managed services than bandwidth, and Stripe makes money solving problems rather than moving bits.

The Gold Rush taught us this lesson: Levi Strauss made a fortune selling denim to miners while the smart money avoided panning for gold.

The same dynamic is emerging in stablecoins. Infrastructure is becoming table stakes. The real value lies in orchestration. Mastercard recently highlighted startups building stablecoin orchestration as key to the future of digital assets. Just this month, a fintech consortium launched an open stablecoin payments platform focused on pull payments, recurring subscriptions, and multi-party settlement. Why? Because stablecoins lack the coordination and authorization layers businesses need.

Simply providing raw pipes isn't enough. The value lies in automating and orchestrating flows on top of those pipes.

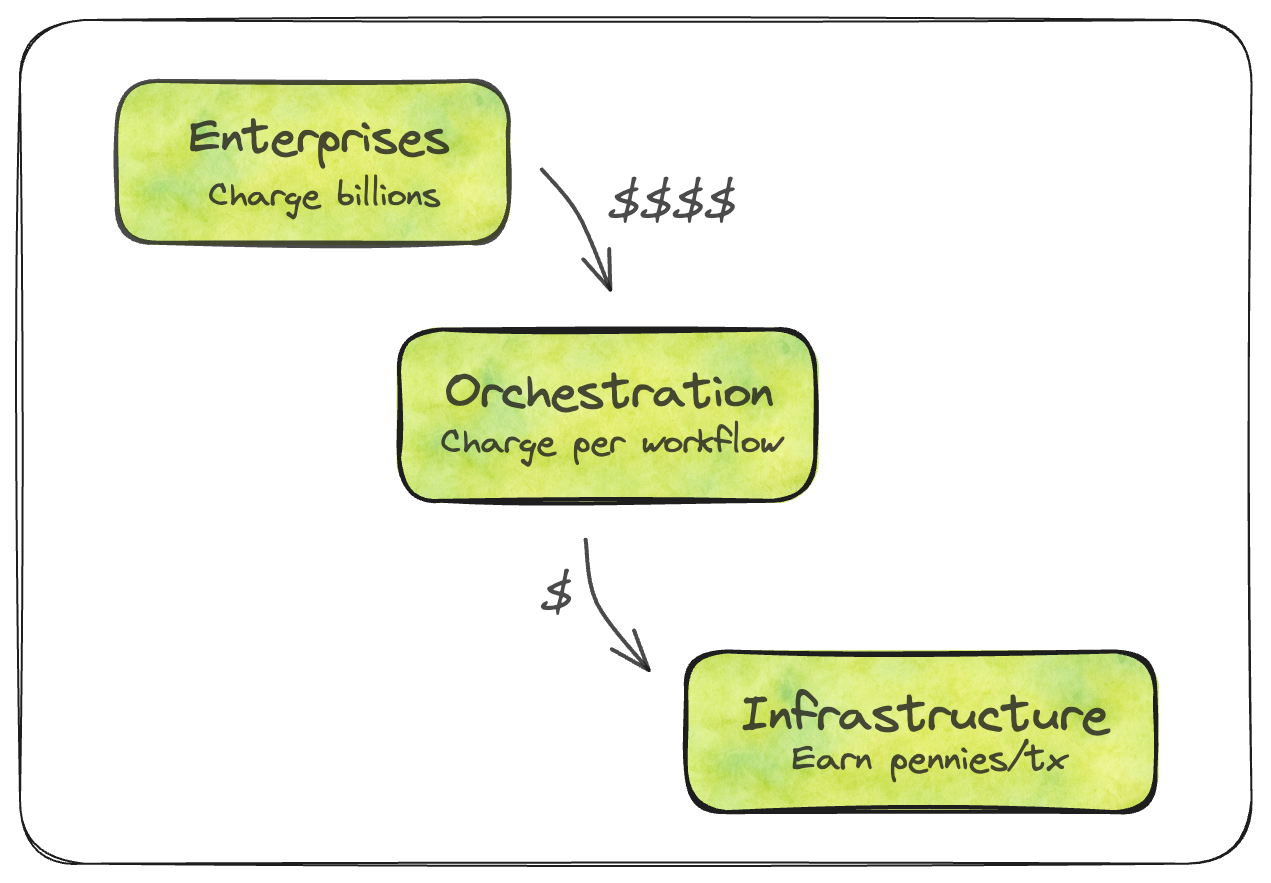

A company that sets up automated subscription billing or programmatic treasury yield strategies isn't just a casual user of an L1. It's deeply integrated with the orchestration service enabling those features. An orchestration platform might charge a few basis points per execution, but if that eliminates a manual process that used to cost hours, it's easily justified. Meanwhile, the blockchain gets its fraction-of-a-penny gas fee. Over time, more value concentrates at the orchestration layer rather than the transport layer.

The Orchestration Advantage

What Automation Unlocks

Crypto transactions today are one-off and manual, while traditional finance runs on automation. The subscription economy ($650B in 2020, projected $1.5T by 2025) relies on recurring billing, and lending uses automated installments—all built on pre-authorized transactions that just happen.

Crypto has never had a reliable analog for this, but that's changing. New Ethereum upgrades will let wallets have built-in "if/then/when" rules that execute automatically. Programmable money.

This unlocks the highest-retention use cases: subscriptions that bill in USDC, automated dollar-cost-averaging, and supplier payments that release when goods are confirmed. The user sets the rules once, and the system carries them out.

Critically, this happens non-custodially, meaning funds stay under enterprise control with no black box handling their money. Enterprises won't adopt automation that requires surrendering custody.

This is what separates orchestration from infrastructure: infrastructure gives you a fast, cheap transaction, while orchestration gives you an automated business process.

Why Economics Favor Orchestration

Infrastructure earns micro-fees per transaction. Orchestration charges for the problem solved. Save a company $50 in bank fees? Generate $500 in yield? Taking a few dollars or a percentage is entirely reasonable. Far more attractive than scraping fractions of a cent in gas fees.

Orchestration compounds. Platforms layer on services, build customer relationships, and amass ecosystems of integrations that become hard to displace. A business that embeds orchestration into its treasury operations faces real switching costs. Re-training staff, altering workflows, potential downtime. That stickiness translates into durable margins.

You might ask: won't chains just build orchestration themselves? History suggests otherwise. AWS tried to compete with every SaaS built on its infrastructure, and most failed. Stripe could have been built by Visa, but it wasn't. Specialization wins.

Following the Real Money

Over the next five years, hundreds of billions in enterprise payment flows will move on-chain. The chains processing those transactions will earn pennies. The orchestration layer making those flows possible will earn dollars. The question isn't whether stablecoins will eat traditional payments. It's who captures the value when they do.

The winners will be those who solve the messy operational challenges, eliminate six-step manual processes, and ensure a stablecoin payment can be as simple as a direct deposit.

Payment chains and stablecoin issuers racing for liquidity are crucial. But they're increasingly the commodity layer. The real gold is buried in the orchestration layer that sits above, where user experience meets workflow integration, where one-click payments replace manual finance chores, and where solving a $152 billion pain point earns you a seat at the budget table.

That's the opportunity in this digital gold rush. Not in running the fastest chain or issuing the most stablecoins. But in building the orchestration infrastructure that makes it all actually work. The picks and shovels that enable the miners to dig. The tooling that turns stablecoin rails into usable business processes. In the end, orchestration is the name of the game.