The Ah-ha Moment: Manifesto Part 2

In the fall of 2023, we discovered a scrapped Ethereum improvement proposal from October 2020 that would allow us to rewire onchain accounts, powering them with tradfi mechanics that were crucially missing.

Julian Rachman

In the fall of 2023, we discovered a scrapped Ethereum improvement proposal from October 2020 that would allow us to rewire onchain accounts, powering them with tradfi mechanics that were crucially missing.

The absence of this upgrade led to years of topical solutions to account-level problems. Users haven’t been able to simply and securely facilitate actions that truly matter, like direct debit, and extend that functionality beyond the primitive. If we want bank-like user flows onchain, then we need to turn the account—and the account layer—into a Digital Asset Operating System.

It started with a single text message.

I was walking out of a developer meetup in San Francisco. At this point, I had been tinkering with wallet UX and smart account orchestration for a few weeks, and the same frustration kept surfacing — no matter how clever systems got, I was still duct-taping functionality onto a fundamentally inflexible base layer: the EOA.

ERC-4337 had its chance to build a viable alternative to the EOA—and it fell short. It introduced a new stack—bundlers, paymasters, entrypoints—but ended up over-complicating the account layer without rethinking it, and exposing accounts to a whole set of trusted offchain actors it has to depend on to function.

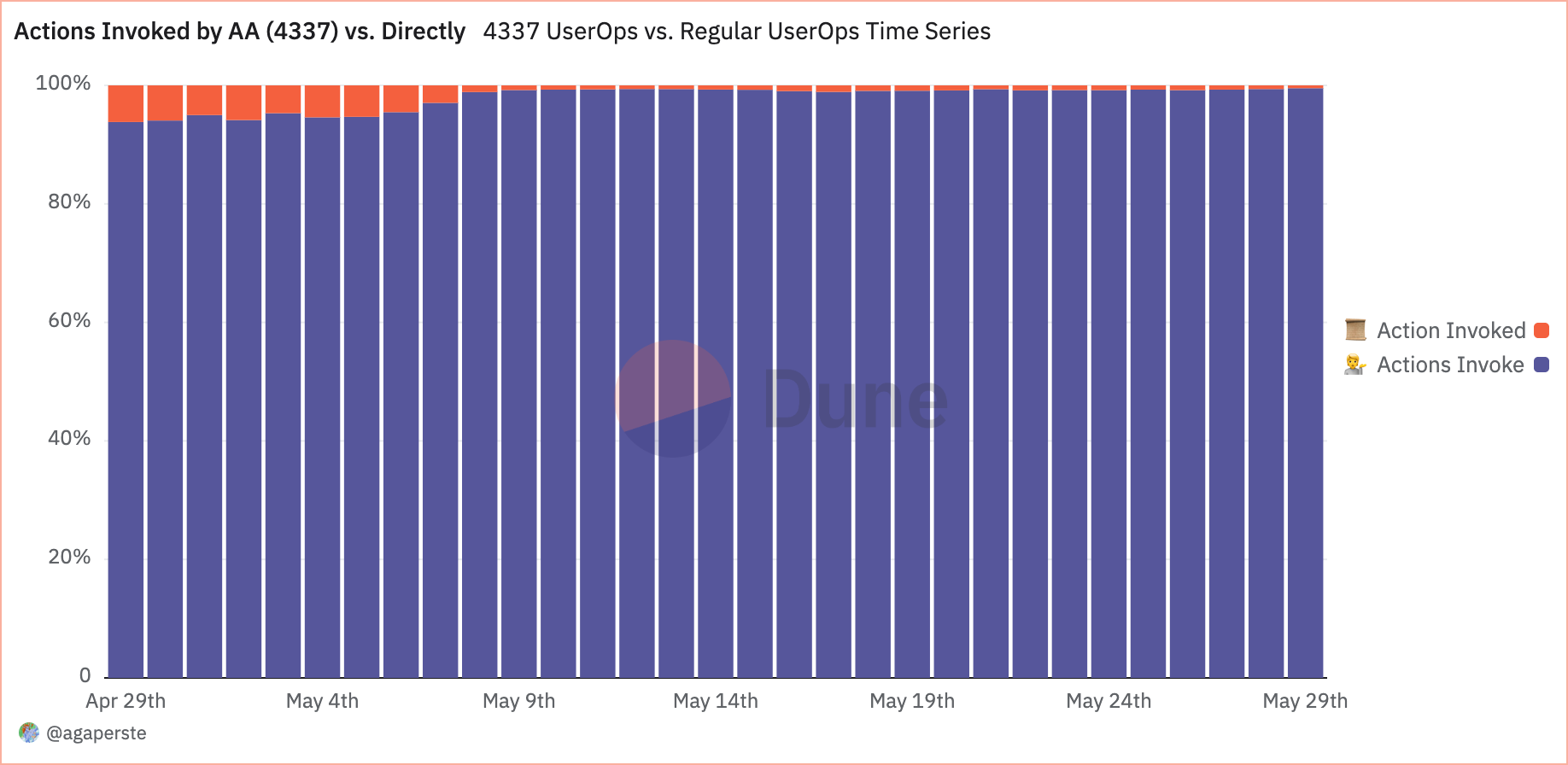

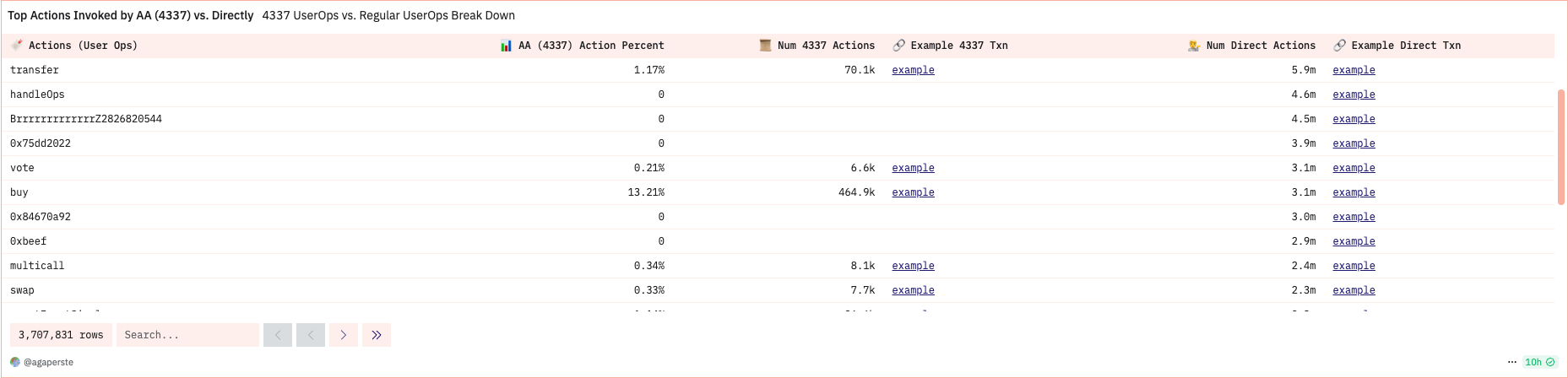

Nearly all onchain value still lives in EOAs, and institutions haven’t budged from key-managed infrastructure like MPC, Secure Enclaves, and HSMs. Around 10% of user actions (i.e., transfers, swaps, etc.) on Base are invoked by 4337-based accounts vs invoked directly by EOA wallets. Boiling it down even more, only 1% of transfers and <1% of swaps are invoked by AA, with a majority still invoked by EOAs.

While messaging a friend about the pain of building new account models, she replied: “You should look into EIP-3074,” and dropped me into a Telegram group chat full of OG builders exploring its potential. That night, I read through it twice. The next morning, I read it again—and this time, it clicked. That was the ah-ha moment.

EIP-3074 proposed something wild: the ability for EOAs to delegate control to a smart contract invoker, without changing the EOA itself. Not migrate. Not wrap. Not re-deploy. Just sign a message, and instantly empower your account to behave in new ways.

That’s when the mental floodgates opened.

What if accounts could pre-authorize recurring transfers without unlimited approvals or sending funds to a vault? What if a user could “authorize” an app the way they authorize Plaid or Stripe—without custody risks? What if every account could become programmable without sacrificing its simplicity?

It was the first time I saw a path to introduce real-world financial mechanics, like pull payments and automated asset movement, into onchain architecture in a way that actually mapped to user expectations.

It’s about time that EOAs learn some cool new tricks.